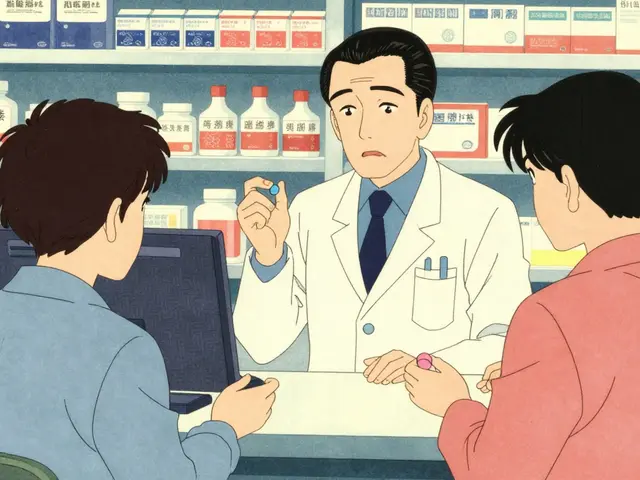

Many people assume that if they have long-term care insurance, it will pay for everything that comes with nursing home care - including medications. But that’s not true. Long-term care insurance doesn’t cover prescription drugs, not even generic ones. This is one of the biggest misunderstandings people have when planning for aging care.

If you or a loved one is in a nursing home, the drugs you take every day - whether it’s a $3 generic blood pressure pill or a $50 brand-name medication - are paid for by something else entirely. And that something else is almost always Medicare Part D. In fact, nearly 8 out of 10 nursing home residents rely on Part D to cover their prescriptions. That’s not a small detail. It’s the main system keeping people alive and stable in long-term care.

Why Long-Term Care Insurance Doesn’t Cover Drugs

Long-term care insurance was never meant to be health insurance. It was built to pay for help with daily living - bathing, dressing, eating, moving around - when you can’t do it yourself anymore. Think of it as coverage for the cost of a caregiver, not a doctor’s visit or a prescription.

California’s Department of Insurance says it clearly: long-term care policies cover custodial care, not medical care. That means room and board in a nursing home, help with hygiene, supervision. But not drugs. Not lab tests. Not doctor appointments. Even if you’re living in a facility paid for by your long-term care policy, the pills you take are handled by a completely different system.

This separation isn’t new. It’s been this way since the 1970s. But things got even clearer in 2006, when Medicare Part D launched. Before then, many nursing home residents paid for drugs out of pocket - or not at all. Now, Part D is the default. And it’s the only thing standing between thousands of people and being unable to afford their medications.

Who Pays for Generic Drugs in Nursing Homes?

Generic drugs make up about 90% of all prescriptions written in nursing homes. They’re cheaper, just as effective, and often preferred by doctors and pharmacists. But who pays for them?

Medicare Part D covers them - and usually at a lower copay than brand-name drugs. For example, a generic diabetes pill might cost $5 a month under Part D, while the brand version could be $40. That difference adds up fast. In 2021, Medicare Part D paid $35.1 billion for nursing home drugs. Medicaid paid $4.8 billion. And out-of-pocket payments? $3.8 billion. That last number? That’s the people who don’t have coverage - or didn’t enroll in Part D.

Here’s the scary part: nearly 9% of long-stay Medicare residents in nursing homes had no detectable drug coverage at all. They were paying for everything themselves, or getting temporary help from charities or state programs. That’s 29,000 people in one year - just in the Medicare population.

And here’s something most families don’t realize: just because a drug is generic doesn’t mean it’s automatically covered. Every Part D plan has a formulary - a list of approved drugs. If your medication isn’t on that list, you might have to wait, appeal, or pay full price. Some plans will cover a non-formulary drug for up to 180 days, but they’re not required to. And many don’t.

The Role of Medicare Part D and Formularies

Medicare Part D is run by private companies - UnitedHealthcare, Humana, CVS/Aetna, Cigna, and WellCare. These are the big five. Together, they cover 78% of all nursing home drug plans. Each one has its own rules. One plan might cover a generic version of a heart medication. Another might not. One might require prior authorization. Another might have a step therapy rule - you have to try a cheaper drug first.

Nursing homes have to keep track of all of this. When a new resident arrives, staff must figure out:

- Which Part D plan they’re enrolled in

- Whether that plan works with the facility’s pharmacy

- What drugs are covered - and which aren’t

- How to file an exception request if the needed drug isn’t on the formulary

This isn’t a one-time task. It’s constant. A 2019 survey found that nursing homes spend 10 to 15 hours a week just managing drug coverage issues. That’s over $28,000 a year in staff time per facility. And that’s not counting the delays in getting meds to residents. On average, it took 3.2 days to get a new prescription filled. Facilities with good systems - like electronic links to Part D formularies - cut that down to under a day.

And here’s the kicker: if a resident switches plans, or if the plan changes its formulary mid-year, the facility has to scramble again. A drug that was covered last month might be dropped tomorrow. No warning. No grace period. Just a note from the pharmacy: “We can’t fill this anymore.”

What Happens When a Drug Isn’t Covered?

Let’s say your mom takes a generic version of a cholesterol-lowering drug. It’s been working fine. Then, the Part D plan she’s on drops it from their formulary. Now, the pharmacy won’t fill it. What happens next?

Her doctor has to choose a new drug - one that’s on the plan’s list. But not all alternatives are equal. Maybe the substitute causes dizziness. Maybe it interacts with another medication. Maybe it’s not as effective. And if the new drug isn’t covered either? The family has to file an exception request. That’s a formal appeal. It can take days. And during that time, your mom might go without her meds.

Part D plans are required to respond to exceptions for nursing home residents within 72 hours. But that doesn’t mean they always do. Some delay. Some deny. Some say “no” and make you go through a second-level appeal. And if you don’t have someone fighting for you - a family member, a social worker, a patient advocate - you might just go without.

Dr. David Grabowski from Harvard Medical School says this is a real problem. “The lack of standardization across plans creates confusion for both facilities and residents,” he says. “And when you’re 85 and confused, you don’t fight the system. You just stop taking the pill.”

What About Medicaid and Dual Eligibility?

If you’re on Medicaid - or qualify for both Medicare and Medicaid - the rules change a little. For Medicaid-only residents, the state pays for drugs directly, usually at cost plus a small fee. But if you’re dually eligible (on both Medicare and Medicaid), you’re enrolled in Medicare Part D. Medicaid doesn’t pay for your drugs - Part D does. And Medicaid only steps in to cover your copayments.

This dual system is messy. People don’t understand it. Nurses don’t always know it. Pharmacies get confused. And the result? People fall through the cracks.

There’s also a growing number of “dual eligibles” - people who are poor enough to qualify for Medicaid and old enough to get Medicare. By 2028, Medicare Part D’s share of nursing home drug spending is expected to rise to 85%. That means more people are relying on Part D. And more people are at risk if formularies change.

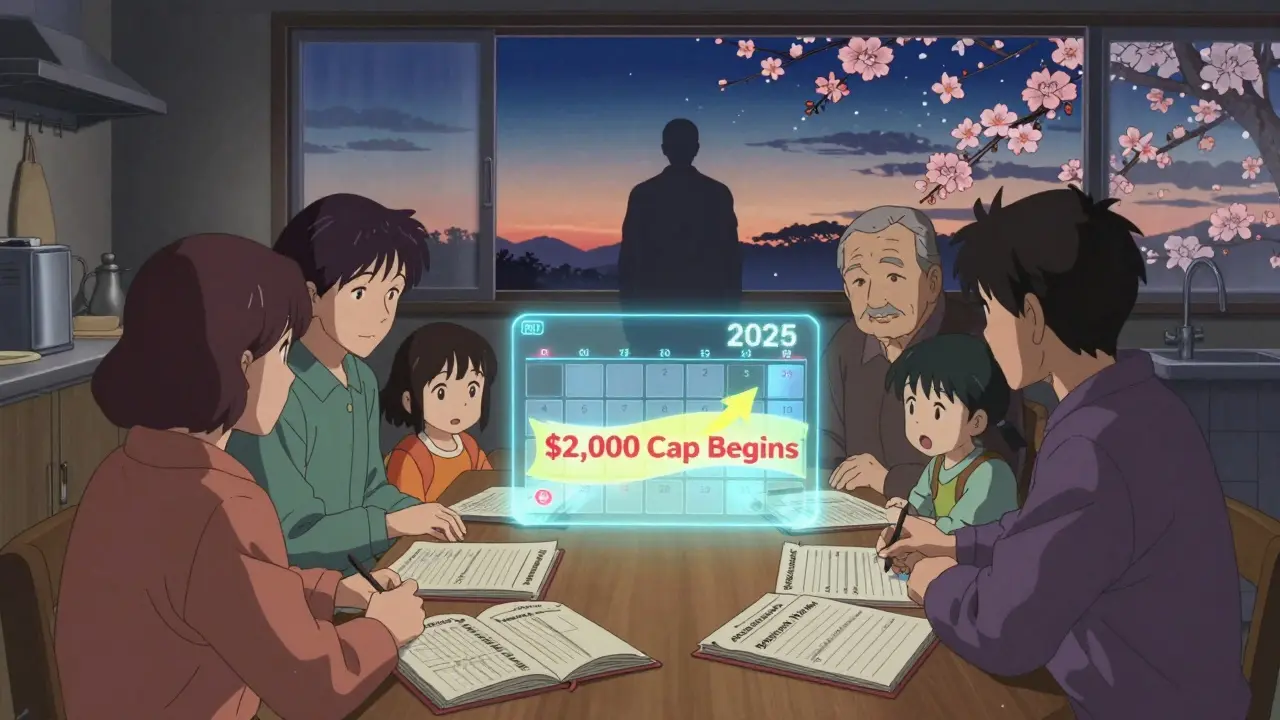

What’s Changing in 2025?

Good news: the Inflation Reduction Act of 2022 is making things better. Starting in 2025, Medicare Part D beneficiaries will never pay more than $2,000 out of pocket for drugs in a year. That’s huge. It ends the “donut hole” - that gap where you had to pay full price after hitting a certain spending limit.

Also, vaccines will be free. And CMS now requires Part D plans to cover all drugs on the official Medicare formulary for nursing home residents. That means fewer surprises. Fewer denials. More consistency.

But here’s the catch: even with these changes, formularies still vary. Plans can still require step therapy. They can still limit quantities. And they can still refuse to cover a drug if they think it’s not medically necessary - even if your doctor says otherwise.

What Families Should Do Now

If you’re helping someone in a nursing home, here’s what you need to do - right now:

- Find out which Part D plan they’re enrolled in. Ask the facility’s social worker or pharmacist.

- Get a copy of that plan’s formulary. Most plans have it online. Call customer service if you can’t find it.

- Check every medication your loved one takes. Is it covered? Is there a generic version? Is there a step therapy rule?

- If a drug isn’t covered, ask about an exception. Fill out the form. Get the doctor to write a letter of medical necessity.

- Keep a binder or digital file with all this info. Update it every time there’s a change.

- Don’t assume anything. Even if a drug was covered last month, it might not be today.

And if you’re considering long-term care insurance? Understand this: it won’t cover drugs. You’ll still need Medicare Part D - or another drug plan - to pay for them. Don’t buy a policy thinking it’ll handle everything. It won’t.

The Bottom Line

Long-term care insurance pays for help with daily life. It doesn’t pay for pills. Medicare Part D does. And while Part D has improved access to generic drugs for millions, it’s still a patchwork system. Formularies change. Appeals take time. Coverage gaps still exist. And the people who suffer most are those who don’t know how to navigate it.

Don’t wait until someone is in a nursing home to figure this out. Learn the rules now. Know the plans. Ask questions. Keep records. Because when it comes to medications in long-term care, the system doesn’t work for you - you have to work for the system.

Jason Silva

December 21, 2025 AT 11:04Bro this is why I told my mom to never sign up for that LTC insurance scam 😅 They make it sound like a safety net but it’s just a fancy brochure that says ‘we’ll pay for your bath towel but not your insulin’ 💸🩹

Meanwhile, Big Pharma and the insurance giants are laughing all the way to the bank. They don’t want you to know this stuff. It’s all smoke and mirrors.

And don’t even get me started on how Part D plans drop drugs like they’re hot potatoes. One day your med’s covered, next day? ‘Oops, sorry, we changed the list.’

It’s a rigged game. And the elderly? They’re the pawns. 😔

Theo Newbold

December 22, 2025 AT 19:59The data presented here is accurate but incomplete. The 85% projection for Part D spending by 2028 assumes no systemic reform. The real issue is the fragmentation of coverage between Medicare, Medicaid, and private insurers. The administrative burden on nursing homes is not merely a logistical problem-it’s a structural failure of federal policy design. The lack of interoperability between formularies and pharmacy networks creates unnecessary delays in care delivery, which directly correlates with increased morbidity in elderly populations. This is not a gap in awareness-it’s a gap in governance.

Jay lawch

December 24, 2025 AT 07:34Let me tell you something about the American healthcare machine. It’s not broken-it’s working exactly as designed. The system was built to extract wealth from the old, the sick, and the powerless. Long-term care insurance? A trap. Part D? A shell game with formularies changing like the weather. And who benefits? The CEOs of UnitedHealthcare, Humana, Cigna. Billion-dollar profits while grandmas go without their blood pressure pills because some algorithm decided ‘Step Therapy’ is more profitable than ‘Life.’

They call it ‘cost containment.’ I call it slow-motion murder. They don’t care if you live or die. They care if your drug is on the approved list. And if it’s not? You’re on your own. The government lets them do this because they’re the ones writing the laws. It’s not corruption. It’s capitalism with a stethoscope.

Christina Weber

December 24, 2025 AT 08:29There is a critical error in your statement: Medicare Part D does not cover all drugs for nursing home residents. It covers them *if* they are on the plan’s formulary-and even then, only after prior authorization, step therapy, or quantity limits are satisfied. The phrase ‘Medicare Part D pays for them’ is misleading. It pays for *some* of them, under *some* conditions, for *some* people. Precision matters. Also, ‘nearly 9% had no detectable drug coverage’-this should be cited as ‘nearly 9% of long-stay Medicare residents in nursing homes had no Part D enrollment or supplemental coverage,’ as Medicaid dual eligibles are not included in that statistic. The nuance is essential.

Cara C

December 24, 2025 AT 13:26This is such an important post. I’ve been helping my aunt navigate this mess for two years now, and honestly? I didn’t know any of this until I was deep in it.

It’s terrifying how much you have to fight just to keep someone alive. I had to call the pharmacy three times, get the doctor to write a letter, and then wait 10 days for an exception approval just to get her generic lisinopril refilled.

But I’m glad you laid it all out. People need to know this stuff before it’s too late. I’m sharing this with my whole family. Thank you for the clarity.

Michael Ochieng

December 25, 2025 AT 21:58Coming from Nigeria, I’ve seen how healthcare works differently here-sometimes better, sometimes worse. But this? This is a whole other level of bureaucratic chaos.

Here, if you can’t afford meds, you either go without or rely on community support. In the U.S., you’ve got this massive, expensive, layered system that’s supposed to help… but ends up tripping people up at every turn.

I think the real hero here is the nursing home staff who spend 15 hours a week just fighting insurance companies. They’re the unsung warriors. Hats off to them.

Jerry Peterson

December 25, 2025 AT 23:56Good breakdown. I work in a nursing home admin role and this is daily reality. We have a whole binder just for Part D formularies. We update it every Monday.

One thing I’d add: if a resident switches plans mid-month, we often get hit with a ‘no coverage’ notice for drugs they’ve been taking for years. The pharmacy doesn’t care if it’s been stable for 18 months. Policy change = no fill.

And yes, we’ve had residents go 3 days without meds because the appeal got lost in the mail. It’s not rare. It’s routine.

Orlando Marquez Jr

December 26, 2025 AT 04:57The structural deficiencies inherent in the current Medicare Part D framework are emblematic of a broader failure in the American healthcare policy paradigm. The delegation of drug coverage to private entities with conflicting fiduciary incentives fundamentally undermines equitable access. The absence of a unified national formulary, coupled with the lack of standardized exception protocols, constitutes a violation of the principle of patient-centered care. It is imperative that legislative reform prioritize uniformity, transparency, and mandatory coverage timelines for all clinically indicated medications in institutionalized populations.

Jackie Be

December 26, 2025 AT 14:46we’re filing an appeal today and I’m screaming at the phone with the insurance lady

THIS IS TERRIFYING

someone please tell me how to not lose my mind over this

John Hay

December 28, 2025 AT 09:42My grandma’s on Medicaid and Medicare. They told us Part D pays for her pills. Turns out it doesn’t cover her thyroid med. We had to pay $80 out of pocket last month. They never told us that.

Don’t trust anyone. Not the nurse, not the insurance rep, not the facility. Check the formulary yourself. Write it down. Keep copies. This system will eat you alive if you don’t fight.

Meina Taiwo

December 28, 2025 AT 11:44Generic drugs are covered under Part D-but only if the plan includes them. Always verify. Always document. Always follow up. Simple.